Abraham Lincoln.

Abraham Lincoln.

Having thrown Greece into a quandary, the banksters are now putting the frighteners on Italy; investors are said to be dumping Italian bonds, but why should we, Italians, or anyone else care?

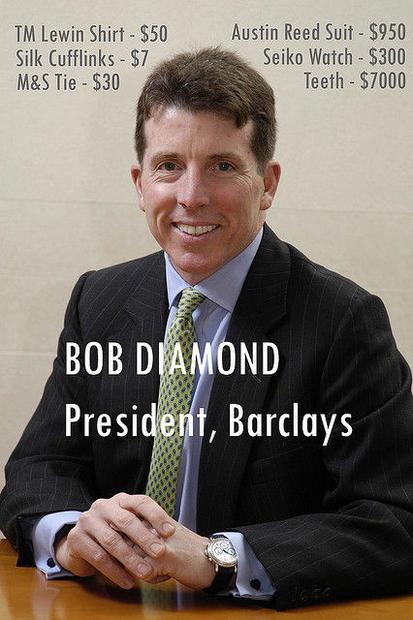

The rhetoric is that without a further bailout, and a further bailout, and a further bailout, trade will grind to a halt, and the world as we know it will come to an end. Anyone who believes that probably also believes Bob Diamond’s claim that banks should aspire to be good citizens.

What though if the world as we know it were to end, or rather, the world as they plunder it? There are those, including financial analyst Max Keiser, who say this would be a good thing, for the rest of us, if not for the banksters. First, let us pause for a moment and take in what they are really saying to us, then decide if it makes sense.

We – meaning us – have to bail out Greece or the European economy will collapse. We must do this by digging into our pockets while at the same time the Greek people must submit to deep cuts in public services.

The money will come out of our pockets, but it won’t go into the pockets of oppressed Greek workers, rather it will go into the pockets of the banksters and their chums who are running pension funds and other funds.

Then we have to bail out Italy. Then Portugal? Who next?

Every time we bail out some economy or other, the people of that country don’t benefit, rather their services are cut, public sector and private sector jobs are lost, and the money goes to the banksters and bond dealers, like the aforementioned Bob Diamond (pictured below) and the charismatic but even more odious Alessio Rastani.

Bob Diamond – the man in the $950 suit who wants us all to tighten our belts so we can pay interest in perpetuity to his bank on the loans he created with a stroke of the pen.

It is important that everyone understands this, because cuts in public services constitute a reduction in real wealth. You may not appreciate that now, but you will when you turn up at an accident and emergency department with a gash in your neck and find there is no doctor there to treat you. Or when your house catches fire, and the operator asks you if you can wait an hour because the only engine within a ten mile radius is out on call.

The extremely expensively dressed Alessio Rastani.

We must not allow the banksters and their political dupes to pull the wool over our eyes, because there is an alternative to bailout, indeed there are many. Firstly, if we bail them out again, it is them and only them who will benefit, the men in the $950 Austin Reed suits. Secondly, if we don’t bail them out, there are alternatives to allowing productivity and trade to stagnate. For one thing, there is barter.

Barter has been around since before money, and our ancestors managed very well with it. While in the modern world it is not suitable for most transactions, there are barter schemes – like this one in the UK – all over the place. This one is based in Florida, and claims at the moment to have members in fourteen countries. Barter between nations on a larger scale is far from unknown, though for any large scale barter, some regular currency is always needed.

Many people will be familiar with LETS schemes – Local Exchange Trading Systems – like LETSLINK UK. This organisation has been around since 1991, and has helped develop the LETS ideology in other countries.

There are local currencies like the Stroud and the more recent Brixton Pound. Finally, there is the big one, governments can break away from the global banking system altogether and issue their own currencies. All nations do this already of course, even the Euro – the designated currency of the global élite on their road to world government – comes in different printings for different countries. What governments must do though is opt out altogether.

When Abraham Lincoln needed to raise money to fight the American Civil War, the banks offered him loans at from 24% to 36%. As the war was partly about abolishing slavery, Lincoln balked at the idea of enslaving the entire nation in order to free a minority, so after casting around for ideas, he hit upon issuing his own money debt-free.

The Island of Guernsey had also issued money debt-free in the 19th Century, and the First World War was fought and won by a bankrupt Britain by the issue of “Bradburys”.

Obviously, the idea has never been popular with the likes of Bob Diamond, and currently only around 3% of money in Britain exists as notes and coins.

Paper money is not entirely without risk; issuing too much can lead to inflation, but the problem Greece, Italy, Britain and the rest of the world in general is currently facing is not too much money but too little. In order to break the stranglehold of the Bob Diamonds and Alessio Rastanis of this world, we must take back our national currencies, and the simplest and best way to do that is for our respective national governments to issue them debt-free.

[The above op-ed was first published November 10, 2011.]

Return To Site Index